#11 How to Budget (Post College)

Building confidence in your financial literacy

Samuel Rudder

Personal finance is one of the most important skills to learn in life. You will always need to deal with finances so wouldn't it be good to understand where & why you're putting your money. It's a shame that academia doesn't require classes centered around money but nonetheless Your Older Brother Sam is here to save the day. Lucky for you, I am very open with how I allocate my finances & want you to succeed in your financial journey as well! Here is what I've learned so far since I've graduated school.

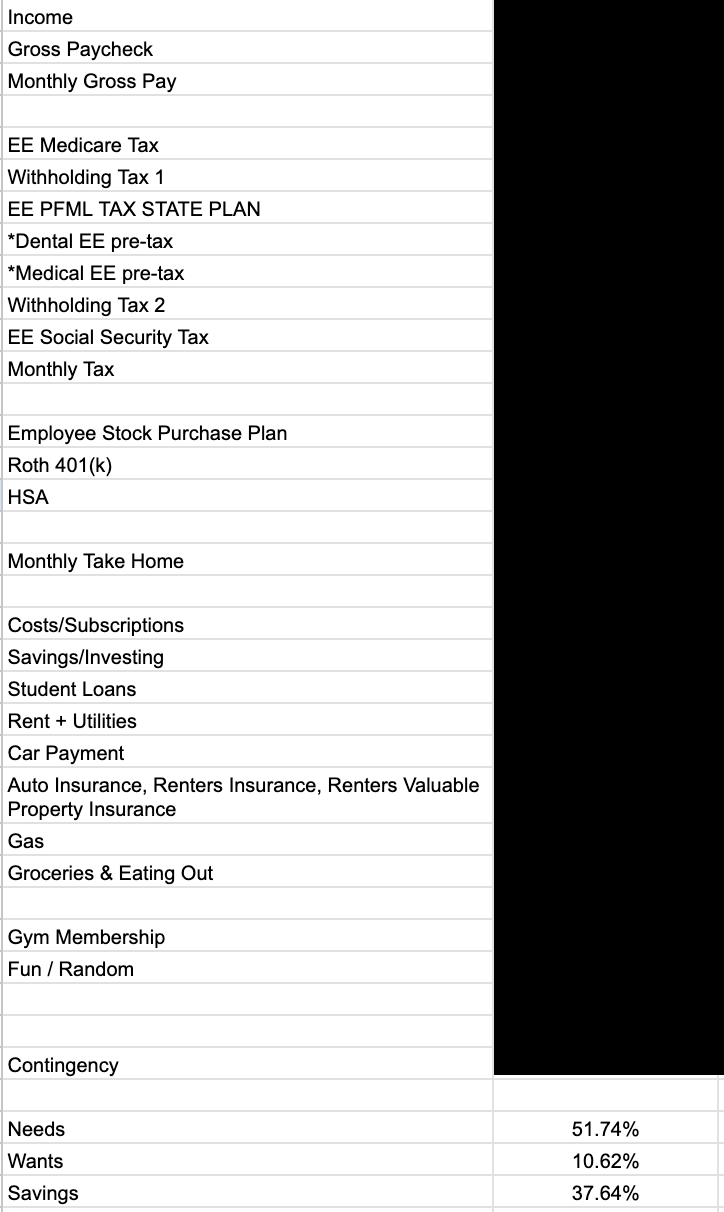

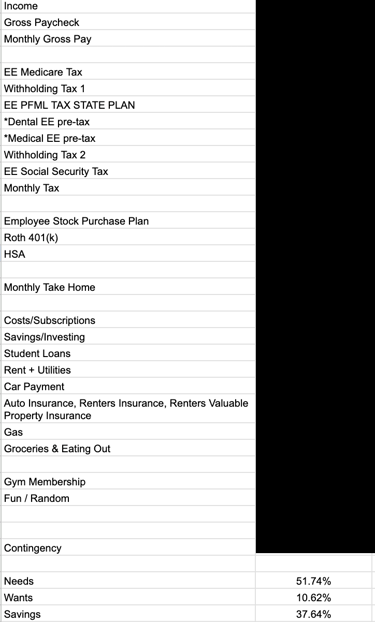

Below is a screenshot of the monthly spreadsheet that I use to track my expenses:

First, I have my total income, I divide by 26 to calculate my gross paycheck because I am paid every two weeks, then I divide my total income by 12 to determine my monthly gross pay.

I highlight all the taxes that I pay then highlight additional funds that will come out of my paycheck like a Roth or Traditional 401k, Health Savings Account (HSA), or Employee Stock Purchase Plan (ESPP). Let me explain all three & why I do each!

Company 401k match

A 401k is a company-sponsored retirement account. For a number of companies, they will provide a 401k match. What that means is based on how much of your paycheck you contribute to your 401k, the company will match it up to a certain figure. At my company, if I contribute 5% of my paycheck, they will match 4%. So, in total, I will have 9% of my paycheck going to this retirement fund with only paying 5% of it myself.

There are two types of 401k's: traditional & Roth. For a traditional 401k, funds are taken from your paycheck pre-tax, grow tax-deferred, then it's taxed when you take the funds out of the account. For a Roth 401k, the money is added to the account after it is taxed, grows tax-free, then these funds are tax-free at retirement. My preference is always Roth because I want my money's growth to be tax-free down the line.

Health Savings Account (HSA)

An HSA is a valuable account to contribute to. This account allows you to pay for medical expenses. You can invest in an HSA with pre-tax dollars, it grows tax-free, & you can withdraw it tax-free. Regardless of your income, you can contribute to an HSA. It's a no brainer. For 2025, the maximum contribution to the account is $4300 for an individual. If you spread this over 26 paychecks, it comes to $166 per paycheck.

Employee Stock Purchase Plan (ESPP)

An ESPP is a company-sponsored program that allows employees to purchase the company's stock at a discounted rate. For example, if the stock price is $100 per share, your company might instead charge you $85 per share. Therefore, your initial return on investment is 17.6% in that scenario. However, it's not always guaranteed you will profit as the company stock has the ability to decrease.

Next, let's focus on how to allocate your take home pay. I divide it into 3 sections: Needs, Wants, & Savings/Investing.

Needs

Needs are fairly straight forward. They're needs to survive: rent/mortgage & utilities, minimum debt payments, insurance, gas, groceries.

Wants

Wants are nice to haves. They're non-essential for living. A fancy gym membership, Amazon purchases, Uber & beers for a night out on the town.

Savings/Investing

Saving & investing are the bread & butter to financial freedom. It's important to make your savings work for you through outlets such as high yield savings accounts, the stock market, real estate, etc.. If you just keep your money in your bank account with a 0.01% interest rate, you're actually 'losing' money due to inflation.

Now there are several budgeting strategies one can use so I'll walk you through three of the main ones!

50/30/20

The 50/30/20 method is a budgeting strategy where you spend 50% on needs, 30% on wants, & 20% on saving/investing. I think it's a good starting point but personally I like to minimize wants as much as possible, therefore, I follow 50% on needs, 10% on wants, & 40% saving/investing.

Zero-Based Budget

The zero-based budget is where every dollar of your income is assigned a specific purpose, leaving a balance of zero at the end of the month. In my spreadsheet, I basically do this, however, I do have a contingency bucket for if I overspend in a particular bucket.

Pay Yourself First

The pay yourself first method is for prioritizing savings & investing before budgeting for expenses. For example, you have an agreement with yourself that each paycheck so you will first invest $250 in the stock market before you consider any expenses you might have. This promotes saving & investing for your future.

To summarize, it's tough to go wrong so it's up to you to decide what works best for YOU! I personally do a combination of all three. First, I invest X amount of dollars each paycheck, then I have certain "buckets" for my spending & I track how I do each month, & finally I categorize my needs, wants, & savings to better understand how I am doing. Ultimately, my goal is minimize my needs & wants so I can prioritize my savings which I invest. My next post will talk about how to invest your savings as it's a necessary step in order to build your financial portfolio. Let me how if this was helpful & I can't wait to help you build your future!

© 2024. All rights reserved.